American data analytics and consumer intelligence company J.D. Power recently released the results of the J.D. Power 2021 U.S. Dealer Financing Satisfaction Study. In the study, GM Financial ranked below the industry average in both the Captive – Mass Market segment and the Lease segment.

![]()

The J.D. Power 2021 U.S. Dealer Financing Satisfaction Study is based on survey responses from 2,992 auto dealer financial professionals. The study was fielded between May and June of the 2021 calendar year, and measures auto dealer satisfaction in six different segments. The results are then tabulated in a 1,000-point scale, providing a ranking among the institutions studied.

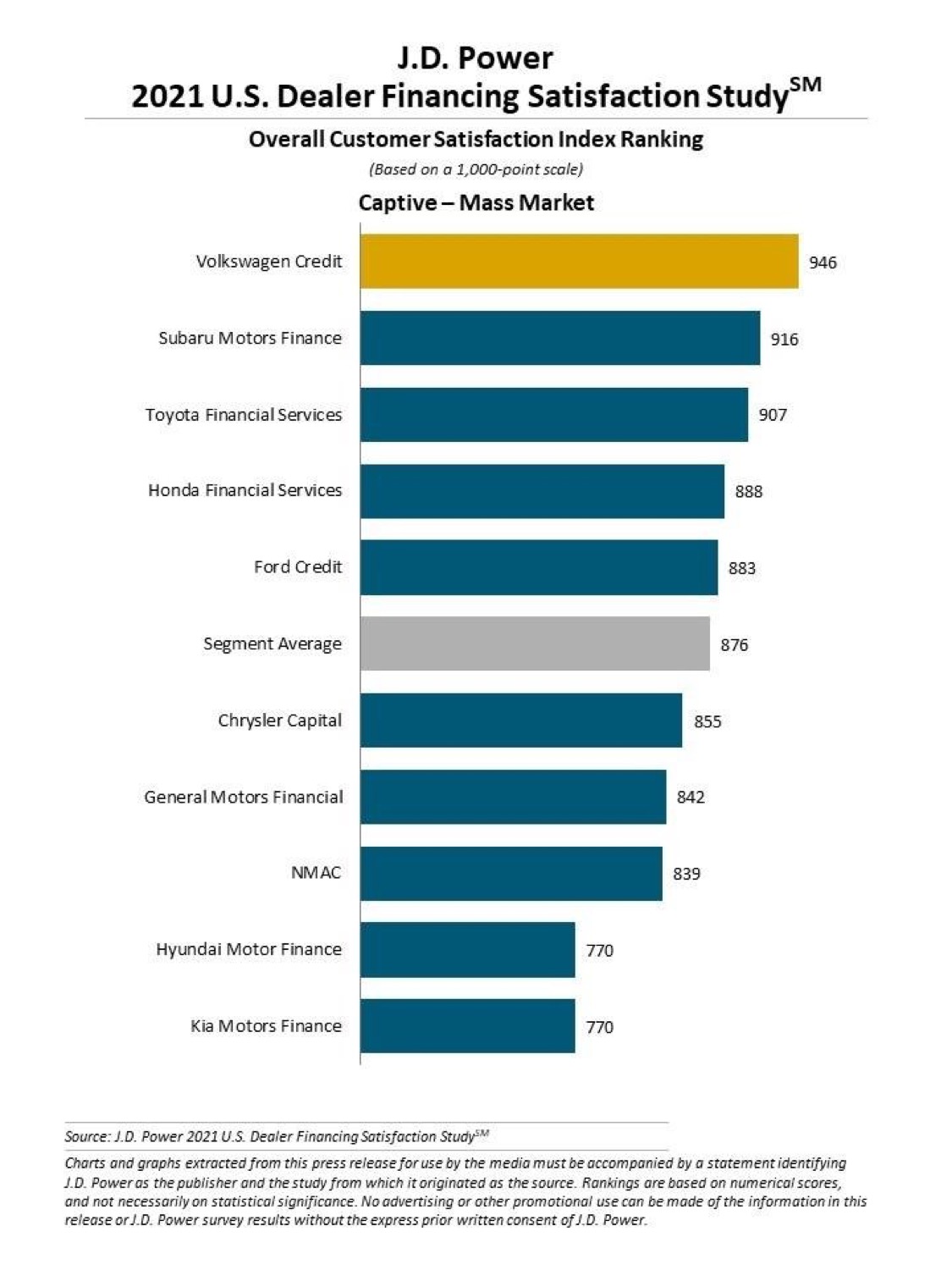

GM Financial was ranked in two of the segments. In the Captive – Mass Market segment, GM Financial scored 842 points, placing it eighth among 11 institutions studied, between Chrysler Capital, which scored 855 points, and NMAC, which scored 839 points. The segment average was 876 points, while the segment leader was Volkswagen Credit with 946 points.

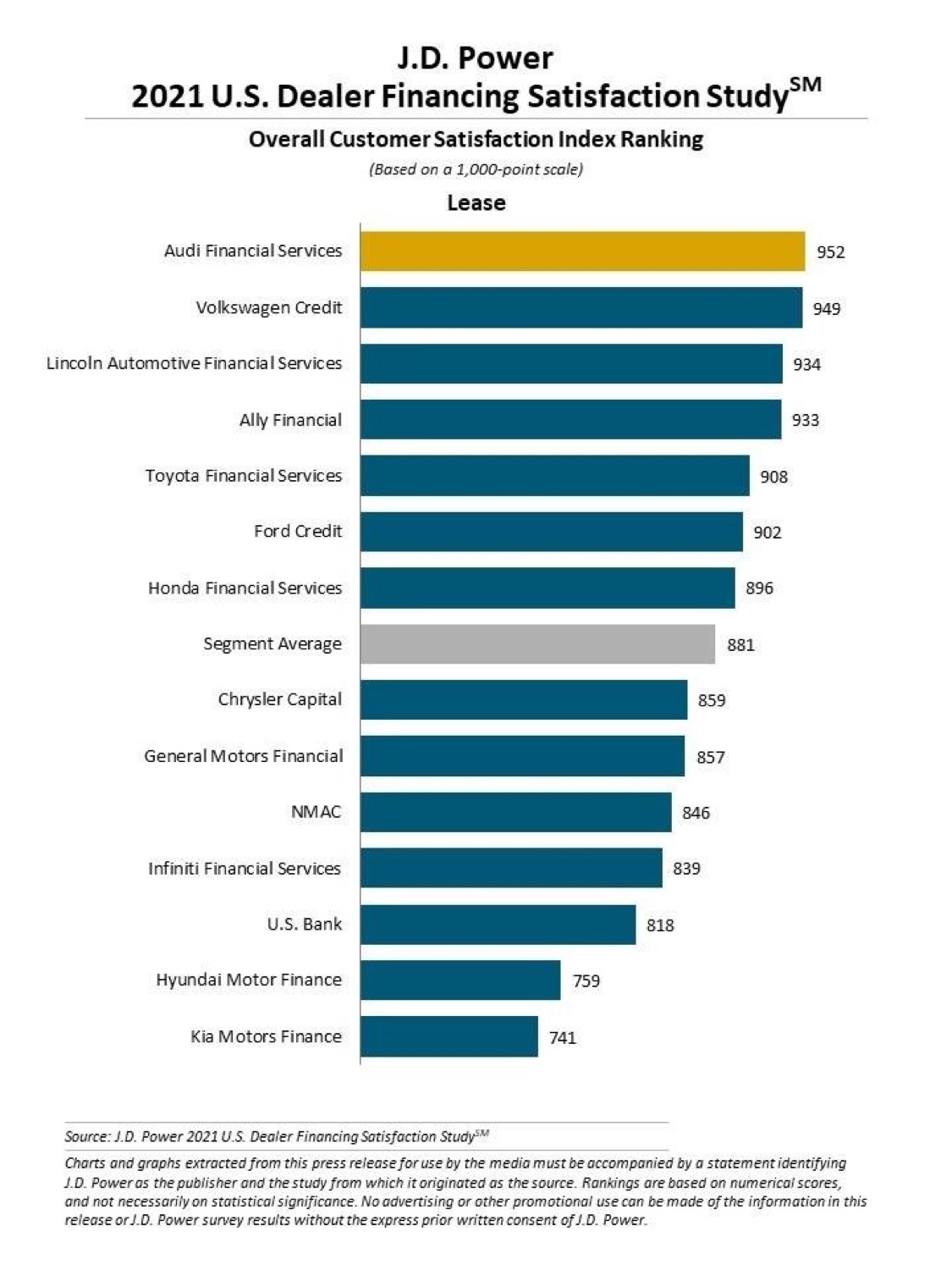

In the second segment, Lease, GM Financial was tenth among 15 institutions studied with 857 points, once again placing between Chrysler Capital, which scored 859 points, and NMAC, which scored 846 points. The segment average was 881 points, while Audi Financial Services topped the segment with 952 points.

“Auto dealers who maintain transactional relationships with lenders, spreading their business across multiple institutions without establishing go-to relationships have significantly lower levels of satisfaction with their lending partners,” said director of automotive finance intelligence at J.D. Power, Patrick Roosenberg. “In this market, where rates are low and new vehicle sales volumes remain significantly suppressed, captive and non-captive lenders who want to stay competitive need to set themselves apart by forging close relationships with dealers through their sales reps, retail credit staff and funding.”

Earlier this year, GM Financial announced that it would stop end-of-lease purchases for non-GM dealers in order to provide participating GM dealers priority in terms of access to vehicle reentering the market, thus hopefully providing GM dealers with greater inventory as the global microchip shortage drags on. Earlier, in May, GM Financial offered lease extensions to customers as the chip shortage hit new-vehicle availability.

Subscribe to GM Authority for more GM Financial news and around-the-clock GM news coverage.

Comments

It looks like I’m not the only one who isn’t satisfied with GM financial. They leave a lot to be desired when it comes to customer service. On August 2, I asked them to send me a copy of my property tax bill that my town sends to them. I have not received it. On September 8, I called again and still have not received it. I have gone through this scenario every year for many years with my GM leases. How long does it take to make a copy of my tax bill and either email it to me or mail it to me?

Just go to the county Treasurer as they are the ones who have your values that are sent out.

Go to your town tax collector and get a copy?

Went shopping for my wife a vehicle. GM financial wanted a 780 credit score. Even with my 811 credit score GM financial wanted to play the money down game to reach 0 percent financing. Ford only wanted a 650 credit score and nothing down. Due to the chip shortage, If you are currently in a lease with Ford, they will give you an extra 12k miles, full bumper to warranty with unlimited miles for another year, free brakes and oil changes. If you are currently in a GM lease they will only extend your lease 6 months and offer nothing else. Through this I learned that not all reports are nonsense. I can honestly see why Ford/Lincoln credit is ranked #1 every year.